When someone sits across from us at MyMoneyMedic drowning in mortgage stress, we see a pattern that repeats too often to be random.

It’s not one dramatic moment. It’s a sequence.

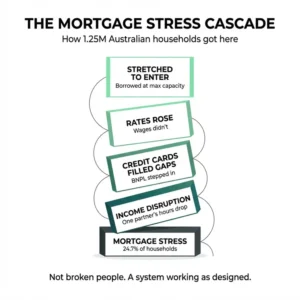

They stretched to enter the market because everyone said “get in now or you’ll be locked out forever.” They borrowed at the top of their capacity because property “always goes up.” Then rates rose. Costs rose. Wages didn’t.

Credit cards filled the gaps. Buy Now Pay Later stepped in. Tax debt lingered. The mortgage remained untouchable.

By the time they reach out for help, they’re emotionally exhausted. And they blame themselves.

That’s the moment we know the system isn’t broken. It’s working exactly as designed.

The System Produces the Outcome It Was Built For

Banks profit from larger loans over longer terms. Property demand benefits from urgency and FOMO. Household debt fuels economic growth.

When families are leveraged to the edge, stressed, and dependent on continued growth to stay afloat, that isn’t an accident. It’s an outcome.

As of November 2025, 24.7% of Australian mortgage holders are classified as “At Risk” of mortgage stress. That’s 1.25 million households where mortgage repayments consume a dangerous portion of income, leaving minimal buffer for life’s inevitable disruptions.

The dream only works if nothing goes wrong for 30 years.

Life doesn’t work like that.

Normal Life Exposes Maximum Leverage

The most common trigger we see isn’t dramatic. It’s income disruption.

One partner goes on parental leave. One income drops due to job change or redundancy. A small business owner has three slow months.

That’s it.

Suddenly, a household that “qualified comfortably” can’t breathe.

Most families don’t borrow based on surplus. They borrow based on maximum serviceability. Two full incomes assumed. Minimal lifestyle change assumed. Rate buffers that feel theoretical until they aren’t.

When one income softens, the margin disappears.

The mortgage was manageable as long as both engines were running perfectly. That’s the fragility.

Roy Morgan’s research confirms that unemployment has the largest impact on income and mortgage stress. Yet affordability assessments assume two full-time incomes remain stable indefinitely.

Among lower socio-economic groups, full-time employment among mortgage holders fell by 11.6% year-over-year. Employment assumptions collapse quickly for vulnerable households.

The Banking Assessment Disconnect

Here’s the uncomfortable truth about affordability assessments.

Most people hear: “You can afford this mortgage.”

Banks are calculating something different.

Income is treated as fixed and ongoing

Banks look at your current declared income and assume it keeps flowing, unchanged, forever. Full-time salary? Assumed stable. Bonus or overtime? Partially counted. Side gigs? Sometimes ignored.

Reality: Income isn’t guaranteed. Promotions stall. Hours get cut. Businesses fluctuate. Parental leave happens.

Expenses are treated as generic or minimal

Banks use broad expense categories, not your actual spending. They assume a “basic lifestyle” number for groceries, utilities, insurance. Car loans, childcare, school fees, subscriptions? Factored in minimally or ignored.

Reality: Day-to-day living costs are higher than these benchmarks and add up quickly.

Stress tests are theoretical

Banks might add a 2-3% buffer for interest rate increases. But it’s applied to the mortgage only, not your total household cashflow. It assumes you adjust perfectly without real-life friction.

Reality: Small rate rises plus normal life expenses equals immediate pressure, not a buffer.

Australian banks routinely approve loans at 5-7 times annual income. The average home loan debt is now $327,514 according to NAB’s 2024 data, while average household gross disposable income was only $139,064.

Debt is growing twice as fast as income.

No human psychology is accounted for

Banks calculate numbers. They don’t account for financial stress impacting decisions, emotional spending, or risk tolerance.

Reality: Even when clients can technically make payments, the mental load is crushing. Sleep, focus, relationships all suffer.

The formula answers: “Could this borrower service a loan under ideal conditions?”

Not: “Can this household live, save, and respond to life while paying this mortgage?”

That gap is exactly where stress builds.

The Tax Incentive Amplifier

Negative gearing by property investors reduced personal income tax revenue by $10.9 billion in the 2023-24 financial year. That’s up from $6.7 billion in 2014-15.

That’s $10.9 billion in foregone revenue effectively subsidizing property speculation while first-home buyers compete against tax-advantaged investors.

In 2022-23, about 1.1 million Australians were negatively geared. That’s 49.4% of all property investors gambling on capital gains to offset years of losses.

The Reserve Bank of Australia stated in 2003 that resources and finance are being disproportionately channeled into property investment, with tax effectiveness being an important selling point used by property promoters.

Tax policy, not housing need, is driving investment behavior.

Research by the Australian Housing and Urban Research Institute reveals that most negatively geared investors buy existing dwellings rather than building new homes. The policy inflates prices for existing stock without meaningfully increasing housing supply.

It’s a demand accelerator disguised as a supply solution.

The 5% Deposit Scheme: Solution or Accelerant?

From October 1, 2025, the Australian Government 5% Deposit Scheme was expanded with no income caps, no waitlists, and higher property price caps up to $1.5 million in parts of NSW.

First-home buyers can now enter the market with minimal equity and maximum exposure to rate fluctuations and life disruptions.

The scheme removes Lenders Mortgage Insurance but requires the property to remain owner-occupied with principal and interest repayments for up to 30 years.

If borrowers fail to meet ongoing obligations like losing a job or needing to relocate, the guarantee may no longer apply. They could face paying LMI or additional costs at their most vulnerable moment.

Parliamentary Budget Office modeling shows the scheme is highly sensitive to assumptions around interest rates, house price growth, and default rates. Default rates are projected at 0.3% annually.

This assumes ideal conditions over 30 years. The exact fragility pattern we see collapsing when normal life happens.

The Household Debt Reality

Australian household debt reached a record $3.33 trillion in June 2025. That’s a 6% increase in just one year.

The average Australian household now carries $313,633 in total debt, with mortgage debt alone representing 135% of household disposable income.

Australia has the fifth-highest household debt-to-income ratio among OECD countries at 211%. The average household owes more than twice what it earns annually.

We’re borrowing two years of income to fund our lifestyle and housing.

The debt-to-income ratio hit 182% in Q4 2024, tracking near record highs. This wasn’t an accident. It’s the predictable outcome when banks approve loans at maximum serviceability and tax policies incentivize speculation over genuine housing needs.

The Stress Distribution Problem

Mortgage stress hasn’t eased evenly.

While higher-income households have found relief, stress has actually increased among the lowest two socio-economic quintiles by over 5% year-over-year.

Relief from rate cuts is bypassing the 40% of Australians who need it most.

Even as interest rates dropped, mortgage stress surged in June 2025 to 28.4%. The highest since January 2025.

Why? Because households were borrowing larger amounts, chasing rising property prices with their newfound “affordability.”

The system encourages maximum leverage the moment conditions slightly improve.

Median mortgage repayments peaked at 47.1% of median household income in September 2024 before dropping to 45% by September 2025. Still far above the traditional 30% mortgage stress threshold.

Nearly half of household income consumed by housing before accounting for food, transport, childcare, or savings.

Why People Don’t Stress-Test

It’s not because people are careless.

Optimism bias: We naturally assume the future will resemble the present. Two stable incomes today feel permanent.

Social proof: Everyone else is borrowing big. If your peers are stretching, stretching feels normal.

Lending framework psychology: When a bank says you can borrow $1.2M, most people hear “you can afford $1.2M.” They don’t hear “you can survive $1.2M under ideal assumptions.”

No one models the downside in real terms: Very few borrowers sit down and calculate what happens if one income drops 30%, rates rise another 1-2%, or they need $20k unexpectedly.

They’re shown approval capacity, not fragility thresholds.

The Independent Advice Vacuum

Access to unbiased financial wellness guidance is rare.

Most advice comes from parties with skin in the game. Mortgage brokers earn commissions on loan size. Real estate agents benefit from higher prices. Bank employees have lending targets.

Financial literacy is rarely taught early or practically.

When families need independent perspective on whether they should stretch for that property, where to find it?

The gap between what’s approved and what’s sustainable requires someone to map both scenarios clearly, calmly, without judgment.

At MyMoneyMedic, we map the official bank-approved scenario and the real-life cashflow scenario.

Once clients see the divergence, decisions change. Borrowing less. Building buffers. Planning strategically rather than hoping for ideal assumptions.

The Generational Impact

Today’s policies are mortgaging future generations’ financial and mental wellbeing.

Young Australians entering the market face a choice: stretch beyond comfort or watch homeownership slip away.

The Australian dream has become a 30-year bet that nothing will go wrong.

Babies. Career shifts. Business cycles. Aging parents. School fees. Burnout.

Life transitions are predictable. But our borrowing decisions assume stability.

The problem isn’t ambition. It’s building a 30-year commitment on a 12-month snapshot.

The Path Forward: Clarity Over Leverage

We don’t sit across from people and tell them the system is rigged.

We sit with them and say: “You’re not bad with money. You’re in a high-pressure structure without visibility.”

When we map their numbers clearly, something powerful happens.

They see where the pressure truly sits. They understand their risk exposure. They regain agency.

Once there’s clarity, there’s choice.

The real Australian Dream isn’t just owning a house.

It’s sleeping at night. Not fearing every rate rise. Having buffers. Having options. Feeling in control.

Home ownership can absolutely be part of that dream. But only if it’s aligned with cashflow reality, not social expectation.

What We Believe

The system won’t change overnight.

But individuals can change how they engage with it.

That’s where power comes back.

When someone realizes they’re not broken, that they’ve simply been operating inside a system that rewards maximum leverage, everything shifts.

Not into fear. Into strategy.

When clients stress-test properly, they borrow differently. They build buffers first. They think in cashflow, not just asset value. They prioritize flexibility.

The dream isn’t fragile if it’s built with margin.

At MyMoneyMedic, we’re building a holistic finance health and wellbeing ecosystem to democratize financial wellness solutions. We’re not just another financial advisor.

We’re financial stress specialists focused on data privacy, trust, and care.

Because the real crisis isn’t just about property prices.

It’s about the mental, physical, and emotional toll of carrying debt that looks affordable on paper but crushes people in reality.

And when we help someone see their numbers clearly, map their actual risk, and build a plan with breathing room, that’s when the Australian dream becomes possible again.

Not as a scheme. As a choice.